Battery prices continue to fall so their time will come and with enhanced export rates from ‘Axle’ it’s becoming tempting. If you are installing solar now, you’ll have to choose between micro-inverters, a direct to AC inverter or a battery based inverter/charger. For what it’s worth I’d go for Enphase micro-inverters and leave batteries for later.

Why not batteries now? I suspect these sums will seal the debate.

Let’s work around a hypothetical 10kWh battery costing £3,000. We’re assuming no losses so everything will be worse than shown by this basic maths.

Solar storage

Base line, use the free battery provided by the grid; export for 12p and buy back for 25.5p Here the free battery is charging a holding cost 13.5p per kWh. Think of it as a rental charge for an infinitely large battery that holds your inputs for as long as you like. Zero capital cost to you though so £3,000 in pocket; stick that in premium bonds for 10 years instead? Whatever you do, your battery project has to compare as an improvement over the virtual battery that is ready to use whenever you like.

Solar + Battery; input free, profit £25.5p so 12p better than the free grid battery solution. For 10kWh that’s £1.20 saving per day, so payback takes just under 7 years of surplus energy every perfect sunny day. So, in reality, about 15 years then. Is that fair? What about storing free energy and getting 25.5p worth later for a 3 year payback. Nice idea but that assumes 10kWh every day of the year, even the 200 days of winter. You’d also be directly consuming some of your solar production (practically all of it in winter) so you can more than double this estimate. 7 years? Possible but unlikely. And, sorry to rub this in, there’s still the grid battery available to you so these optimistic sums are based on a fragile platform.

Other interesting ideas

Off-peak storage sold to grid – 7.5p in 12p out – profit of 4.5p. For 10kwh that’s 45p/day. To pay back£3,000 would take 18 years but then more really because the batteries would die before that.

Off-peak storage used next day – 7.5p in 25.5p worth out – a saving over the grid of 18p. For 10kwh that’s £1.80/day. To pay back £3,000 would take 5 years. After that, the next 5 years drops £3,000 into your pocket but then the batteries need changing so it’s gone again. Close! But not overly compelling.

A bit of solar and a bit of off-peak

There’s a seasonal split here for sure. In Summer there is little demand for electricity and in practice, even with no battery at all, bills are pretty much matched by exports. In winter there is significantly reduced solar so the story is all about off-peak storage and we’ve covered that above.

Unfortunately, we have failed yet again to make a compelling case for battery storage. If that leaves you with £3,000 burning a hole in your pocket just consider that the payback time on solar panels is hovering around 3 years so make sure you have enough of them. Your money will do much more for you here.

Here’s a rough example for PV evaluation. Scale up to suit.

£1,400 buys 4 panels with microinverters. (Includes £500 for fitting)

Total 2000Wp

This makes 1,600 kWhrs a year

That’s worth £400

Payback is 3.5 years.

So, there you go. That £3,000 would buy you a nice solar rig and not a battery in sight.

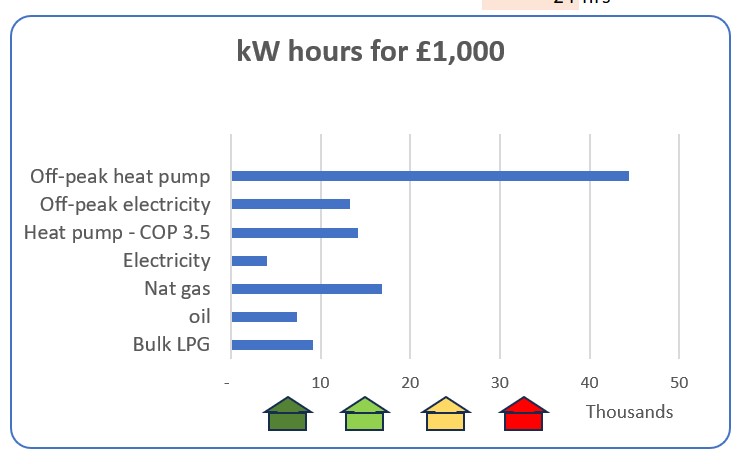

So many people are saying their new heat pump is costing a fortune to run. Well, they run on the most expensive energy available so what did they expect? This chart shows that heat pumps are no cheaper to run than gas boilers, so should you walk away from the idea right now?

Back to the chart though and WOW, look at that. A heat pump running on off-peak electricity will heat most houses for well under £1,000 over the 200 days of winter. So, no, don’t walk away; a heat pump run intelligently can be the best solution by miles.

But where is your house on all this? You can get there by extrapolating from your existing bill. So, say you spend £1,330 on gas (adding another third to that Nat gas bar) you are using about 24,000kW hours which puts you in the yellow house. Looking up to the ‘off-peak heat pump’ line, the same amount of energy would have cost about £500. The conclusion is that for any fuel and any house, a heat pump could halve your bills, but only if run on the cheapest electrcity.

How is that even possible? Well, it’s just simple maths. A typical small heat pump (12kW) consuming 3kW at 7.5p/kWh for 7 hours a night costs a mere £1.52. With a COP of 4 multiplier this makes 16,263kWh over 200 days for a mere £305. That would suit the small and well insulated green house. All this happens at night but we want heat during the day so now let’s talk about storage.The cheap energy has to be stored in water tanks (2,000 litres in this case) and there must be underfloor heating to use every last bit of energy in the tank. To get those cheap night rates you might need to have an electric car too. Any house better than the green house, Passivhaus maybe, will almost run for free. Going back to the yellow house, we’ll need 3,000 litres of water storage and a 17kW heat pump consuming 4.5kW at a total cost of £500. A fundamental point here; the heat pump is running fewer hours and needs to be unusually powerful to supply the energy total so it might need to be bigger than your supplier calculates.

The red house gets more interesting. 4,000 litres of water and maybe two heat pumps for an annual bill of about £600. For a deeper dive into all this have a look at the ‘Absolute ultimate heat pump system for large houses’. This explains how the system is put together along with some interesting enhancements.

What about batteries rather than all this tank business? I think water works better and cheaper but you can see the argument here.

Plugging in the new April price caps and prevailing war driven spikes this is roughly how many kW hours £1,000 buys you. Gas and electricity will be fixed until July but oil and LPG will certainly remain volatile. Oil, for example, has shot up to £1.31 a litre (good chart on Boilerjuice) so if you are living in a big old leaky house, like the red one below, your heating bill will be over £4,000. Extrapolating from the bar of your particular fuel will give a good bills prediction with the orange house giving targets for most people using around 25,000 kW hours a year. As usual, at the extremes, a direct electric resistance heater is the worst thing to turn on (even half as good as oil) while the best strategy is to harvest cheap rate energy with a heat pump and store it in a tank for later use. While that heat pump trumps everything it is notable that off-peak electricity is currently better than oil or LPG; maybe night storage heaters are due for a comeback.

Trying to find a filling station that had any diesel left at all was a bit of a wake-up call; an electric car, with attendant cheap night rates, could lower heating and fuel costs while giving some protection from energy crises. Bi-directional chargers? Still ‘on the way’ but could be just months now so choose your car with care.

If these prices persist into next winter the Government will no longer be able to support the price cap so expect some unpleasant changes.

If this sudden price shock is prompting you to take some action you might take a look at ‘Absolute ultimate heat pump system’ where there may be one or two useful ideas for your heating strategy.

Meanwhile, solar panel prices continue to fall and make even more sense. They pair especially well with a mini-split heat pump which is not only cheap to install (£2,000 ish) but gives a welcome addition of air conditioning during these hot summers.

Cheaper batteries are worth considering although payback times still look long. While export rates are falling the idea of giving access to your battery when the grid is stressed is looking tempting. Check out ‘Axle’ who will pay you £1 for every kW hour they take. For that money they can hammer your battery as much as they like. N.B. Check out their compatible inverter/chargers before you install your PV.

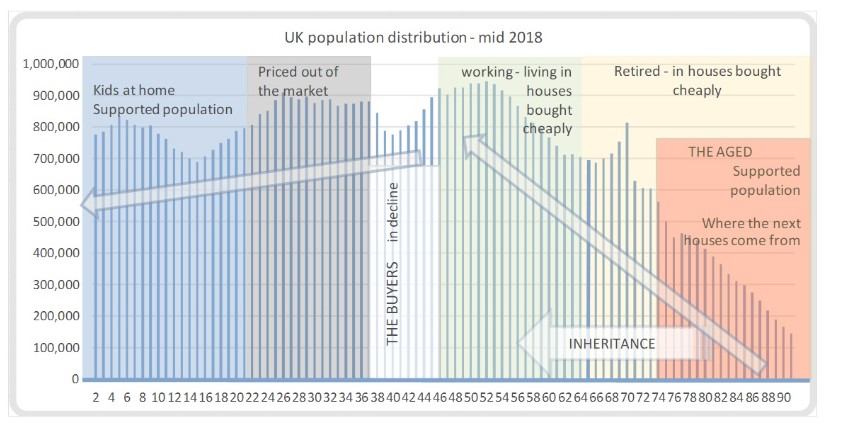

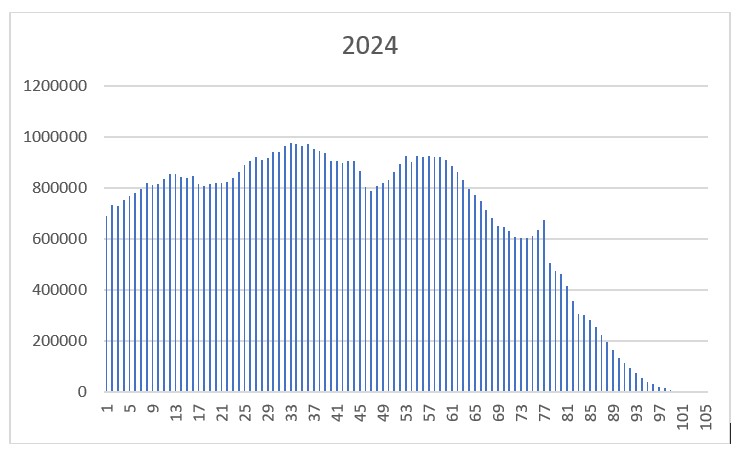

The shape of the UK population in 2018 told a familiar story. The large post-war “baby boomer” cohort — visible as a pronounced bulge in the age distribution — had dominated economic life for decades. This generation benefited from stable employment, affordable housing, rising property values, and strong economic growth. Many accumulated substantial housing equity and later inherited increasingly valuable family homes. Comfortable retirements, foreign holidays, and rising living standards were hallmarks of that era.

Six years later, the 2024 population profile reveals a different picture.

Chart 1: UK Population by Age, 2018

The 2018 age distribution shows the prominent post-war baby boomer bulge (right-hand side). At this point, much of this cohort was approaching retirement, holding substantial housing wealth and representing a dominant economic force.

In 2018, the boomer generation was still economically influential. Many remained in work, while others were entering retirement with significant accumulated assets. Their size amplified their impact on housing markets, healthcare demand, pensions, and consumer spending.

A Declining Birth Rate and an Ageing Nation

The most striking feature of the 2024 chart is the continued fall in birth rates — a trend extending back roughly 60 years. The supply of younger workers is no longer expanding fast enough to support a growing retired population. The UK appears to be shifting from demographic expansion to structural ageing.

Chart 2: UK Population by Age, 2024

By 2024, the baby boomer peak has begun to shrink due to natural attrition, while birth rates remain historically low. The reduction in births highlights a reduced inflow of future workers.

The reduction in the boomer peak reflects ageing and mortality, with the COVID-19 period likely contributing. Notice how the heights of the twin peaks have reversed on the two charts.

The 65-year threshold illustrates that the high flow into retirement will continue for at least another decade. A comparatively smaller working-age population must generate sufficient tax revenue to fund pensions and healthcare. For now, the boomer generation’s children remain numerous enough to shoulder much of that responsibility.

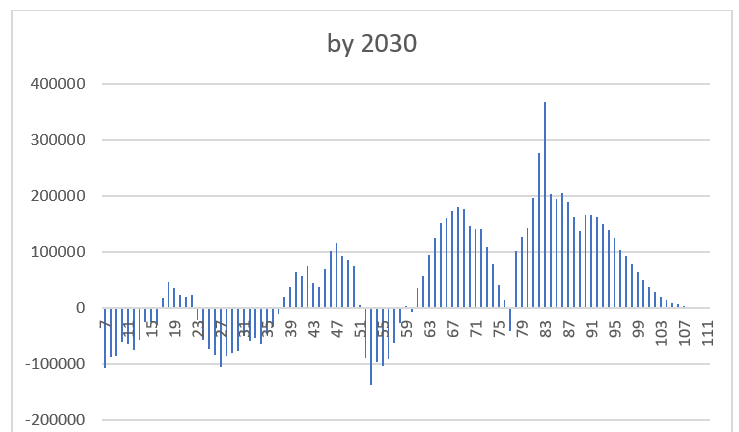

Projecting Forward: 2030

To understand what happens next, we can shift the 2024 age profile forward by six years and measure the differe

Chart 3: Projected Change in Age Groups, 2024–2030

Difference chart showing the change in population numbers between 2024 and 2030. The largest increases occur in older age groups, intensifying pension and healthcare pressures.

Even without adjusting for mortality, the projected increase in older age groups is clear. Given average life expectancy of around 83 years, attrition will reduce the oldest segments, but not before a sustained period of elevated demand on healthcare and pension systems.

The second big block represents the steady swell of future retirees exiting the workforce.

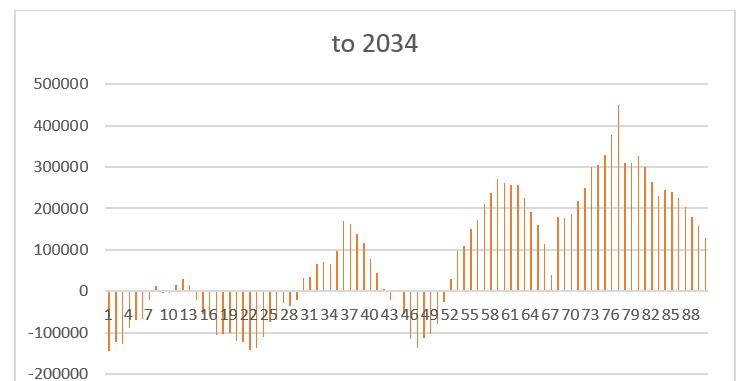

Extending the Projection: 2034

Looking ten years ahead from the 2024 baseline makes the ageing shift even more pronounced.

Chart 4: Projected Change in Age Groups, 2024–2034

Ten-year projection highlighting a substantial expansion in older age cohorts. Figures are measured in hundreds of thousands, underscoring the fiscal significance of demographic ageing.

The scale of the ageing population becomes economically material. Pension liabilities, healthcare costs, and age-related public spending will remain elevated throughout this period.

All pension liabilities are a form of debt – a promise to pay at a future date – and this chart only shows the changes coming. The main blocks from which these figures are derived are still present and significant and yet they are not counted as a component of the national debt.

Wealth Transfer and the Housing Question

One frequently raised concern is whether a wave of property sales will destabilise housing markets as older homeowners pass away. This appears unlikely to produce a sudden glut. Much housing will transfer through inheritance rather than open-market sale. Properties are likely to cascade down the generational ladder.

Over the next decade or two, the UK may experience one of the largest intergenerational wealth transfers in its history. For the boomer generation’s children — currently in their prime working years — this could provide relative financial stability during demographic adjustment.

The Longer-Term Challenge

The deeper structural issue emerges further ahead.

When the boomer generation’s children retire — roughly 25 to 30 years from now — they will be followed by a significantly smaller cohort. If birth rates remain subdued, the tax base may struggle to sustain pensions, healthcare, and public services at current levels.

This challenge is not unique to the UK. Across Europe, demographic pressures are intensifying. Countries such as France face similar trajectories, while Germany and Italy confront even sharper ageing profiles.

A Generation That Shaped the Economy

The defining story is the rise and fall of the baby boomer bulge. At peak working age, it drove growth and prosperity. As it aged, economic momentum slowed, pension obligations expanded, and healthcare demands rose.

For the next decade, relative stability is plausible as wealth transfers offset some pressures. Beyond that horizon, demographic arithmetic becomes harder to ignore.

The UK’s long-term prosperity will depend on how effectively it responds — through productivity gains, workforce participation, immigration policy, technological innovation, and pension reform.

Demography is not destiny. But it sets powerful constraints — and the charts suggest the most significant adjustments are still to come.

In the UK you can drive a light quadricycle on a motorcycle licence. There’s not much to these vehicles so this begs the question – could you actually just make one? I’m thinking pretty much on the kitchen table and using just regular hand tools.

Here the body has a frame made with these aluminium extrusions.

The ‘T’ slots enable panels of polycarbonate and plywood to be easily bolted on or slotted in. With a side profile of 1.2m x 1.2m at this stage it is still easily lifted off the kitchen table and with a plastic chair inside you can already sit in it. What makes it go?

There are loads of ads for electric hub motors for scooters and a pair of these at the back would be perfect. Failing that, a pair of decapitated scooters bolted to the floor would provide power and batteries all in one go. Just make sure you don’t exceed 6kW if you want to keep to a simpler light quadricycle. At the front you could use go-kart parts to provide brakes and steering although the front wheels you chopped off your scooters might do. Even better might be a ready made cyclekart front axle – see link below.

Lights? Just bike stuff, even torches. Speedo? Phone. Wipers? Nah, just prop open the screen. Suspension? Possibly not needed at such low speeds but tennis balls make cheap springs. Luggage? Box at the back doubles as a seat.

So, lots of ideas that might provide inspiration for a fun project and ultimately make the school run interesting and economical.

You might find it hard to tear yourself away from the cyclekart web site. If you are inspired in this direction have a look at the OriginalTwist 3-wheeler here which might tie in nicely. A cyclekart Morgan F4; now there’s an idea. My first car was an F4; great fun.

If you’re building an EV or converting an existing car, why settle for ordinary when you can create something extraordinary? Enter the Emrax 348 electric motor—one of the most impressive motors available today. Whether you’re using one, a pair, or going all out with four, the numbers are jaw-dropping:

Emrax 348 Quick Specs:

Dimensions: 348mm diameter × 110mm depth (about the size of a wheelbarrow wheel).

Torque: 1,000 Nm—nearly as much as a Bugatti Chiron (1,600 Nm), so a pair of Emrax motors surpass it. Of course, the Chiron has a gearbox, but still.

Power: 500 hp per motor (1,000 hp for a pair, obvs). Although output is halved after 2 minutes, that’s more than enough if you’re hitting 100 mph in under 7 seconds.

Max Revs: 4,000 RPM—this limits top speed and influences gear ratios, making it a balancing act between acceleration and top speed.

Design Objective:

Create a modular unit that combines suspension, steering, braking, and drive—all in one elegant package. The idea is to keep it compact and cost-effective, but versatile enough to be used on any corner of the car.

The core of the module is a CNC-machined aluminium plate (approx. 60×40 cm). Mounted to it are:

Unequal-length wishbones shorter upper arms – longer bottom arms bolted at the rear through slots.

A universal hub carrier (e.g. Brypar Motorsport) for flexibility in steering geometry and the strength of Porsche hubs and bearings.

Brake discs mounted close to the plate with callipers fixed directly to it, minimising unsprung weight.

Electric motor + bevel gear drive: Instead of mounting the reduction gear and motor inline (which causes width and cooling problems), we use a bevel gear connected to a short, angled prop shaft. The drive motor is then mounted elsewhere, anywhere along an arc—say, on the rear bulkhead behind the back seats —improving cooling, packaging, and polar moment of inertia. The gear ratio can be changed very quickly just by exchanging the whole bevel gear housing.

The suspension uses a pushrod-actuated rocker linked to a spring/damper mounted along the top of the plate—neatly tucked away and easy to tune.

Performance Examples:

Two-Wheel Drive:

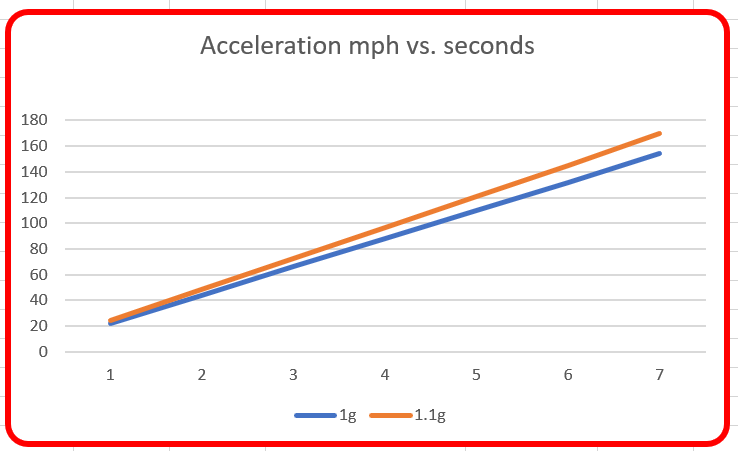

Cap your top speed at 150 mph and the gearing and torque gives around 1.4 tons of thrust at the wheels. If your car weighs more than that—and most EVs do—you won’t hit the 1g needed for a 2.5-second 0–60 mph time although circa 3 seconds would be a reasonable expectation. So while a 1,000hp car will be pretty spectacular, to graduate from supercar to hypercar territory, you’ll need four-wheel drive.

Four-Wheel Drive:

Use all four corners, and with a tyre speed rating limit of 186 mph, you’ll get 2.2 tons of thrust (or 2.67 tons if limiting top speed to 155 mph). With a 2.2 ton car that translates to 0–60 in 2.5 seconds—now we’re talking hypercar credentials. Tyres are usually grippy enough to allow acceleration of at least 1g. The chart below shows how long that takes to reach various speeds. Unfortunately, the faster you go, the more wind resistance bends those lines; even so, 0-100 in 4 seconds looks like a realistic target.

Braking Considerations:

Even with regenerative braking, powerful cars still need strong friction brakes. Freed from the constraints of wheel diameter, the brake disc can be as large as needed—and even have a second calliper. That means you don’t need massive wheels just to fit oversized brakes. Big discs and double calipers make no difference to unsprung weight – perfect.

Final Thoughts:

These integrated modules are perfect for developing a powertrain test mule. Any sturdy hatchback will do. With most of the engineering already solved, you can jump straight into drivetrain testing without reinventing the wheel.

And because they’re stealthy, we’re entering the golden age of Q-cars. That humble Citroën Berlingo sketched above? It could quietly hide 2,000 hp. Why the Berlingo? There’s loads of room in the nose for front motors, even more in the back, and already wide wheels with arches ready to take bigger tyres. Inside, you’ve got ample space for batteries, telemetry, and more. Why sit on the floor of a cramped supercar when a roomy Berlingo is just as quick?

In case you were wondering, the McMurtry Speirling fan car does 0-60 in 1.4 seconds – but then, you can’t get a sofa in the back.

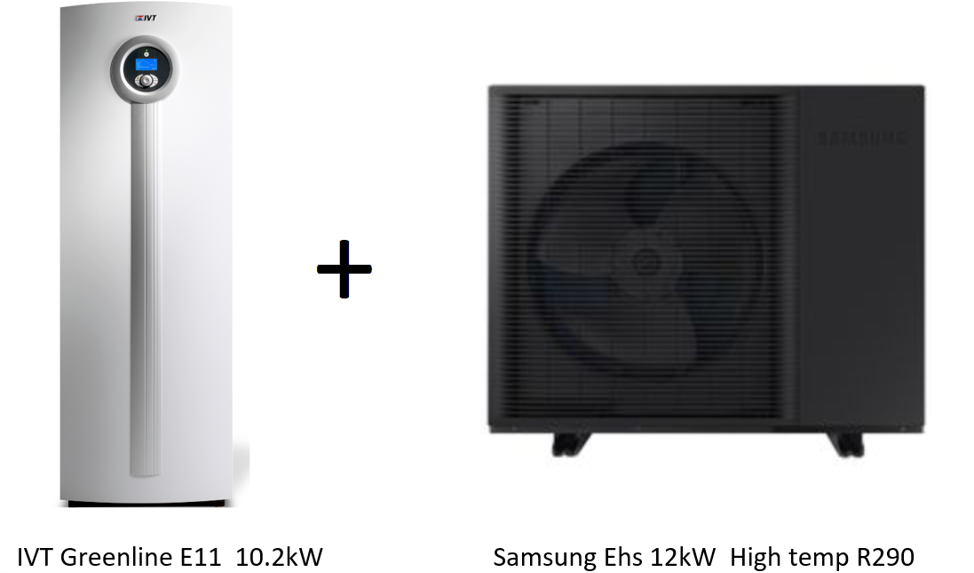

If you fancy the Grand Designs Heating System but need a bit more power for a bigger house then you are in luck; bigger is even better. Rather than scaling up the ground source heat pump we can add one of the latest high temperature air source heat pumps to the mix.

That way we get the best of both worlds with the GSHP taking care of the cheap rate nightshift and the ASHP maximising efficiency with warmer daytime air. Both heat pumps can run together when needed and this layered approach will satisfy the heating seasonal demands of a wider range of houses. Heating with this system is unusually flexible. With energy stored in oversized buffer tanks, the heat delivery is governed by the rate at which it is pumped to the various emitters and not directly determined by heat pump power; it is even possible to exceed the power of the heat pumps for short periods.

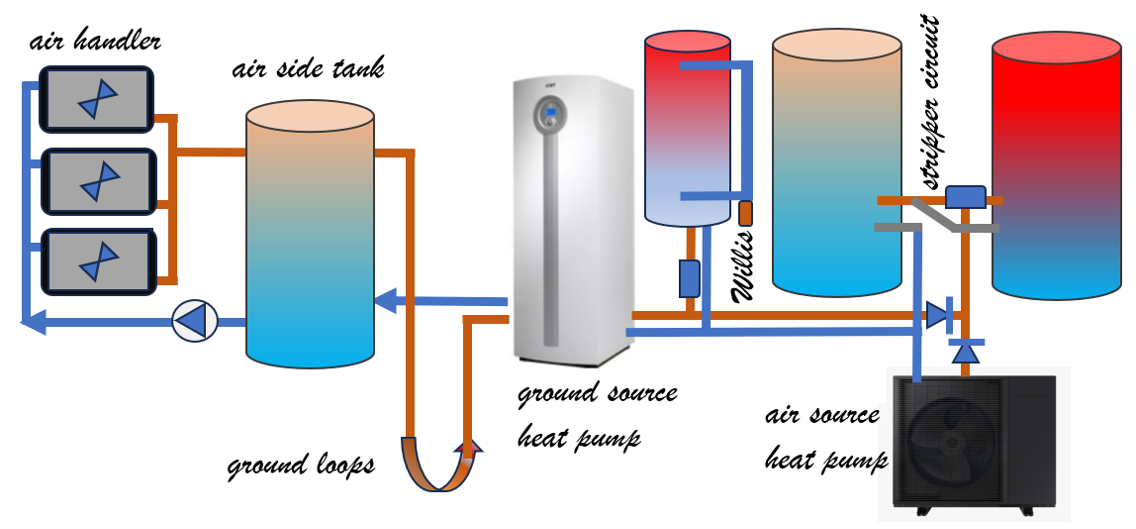

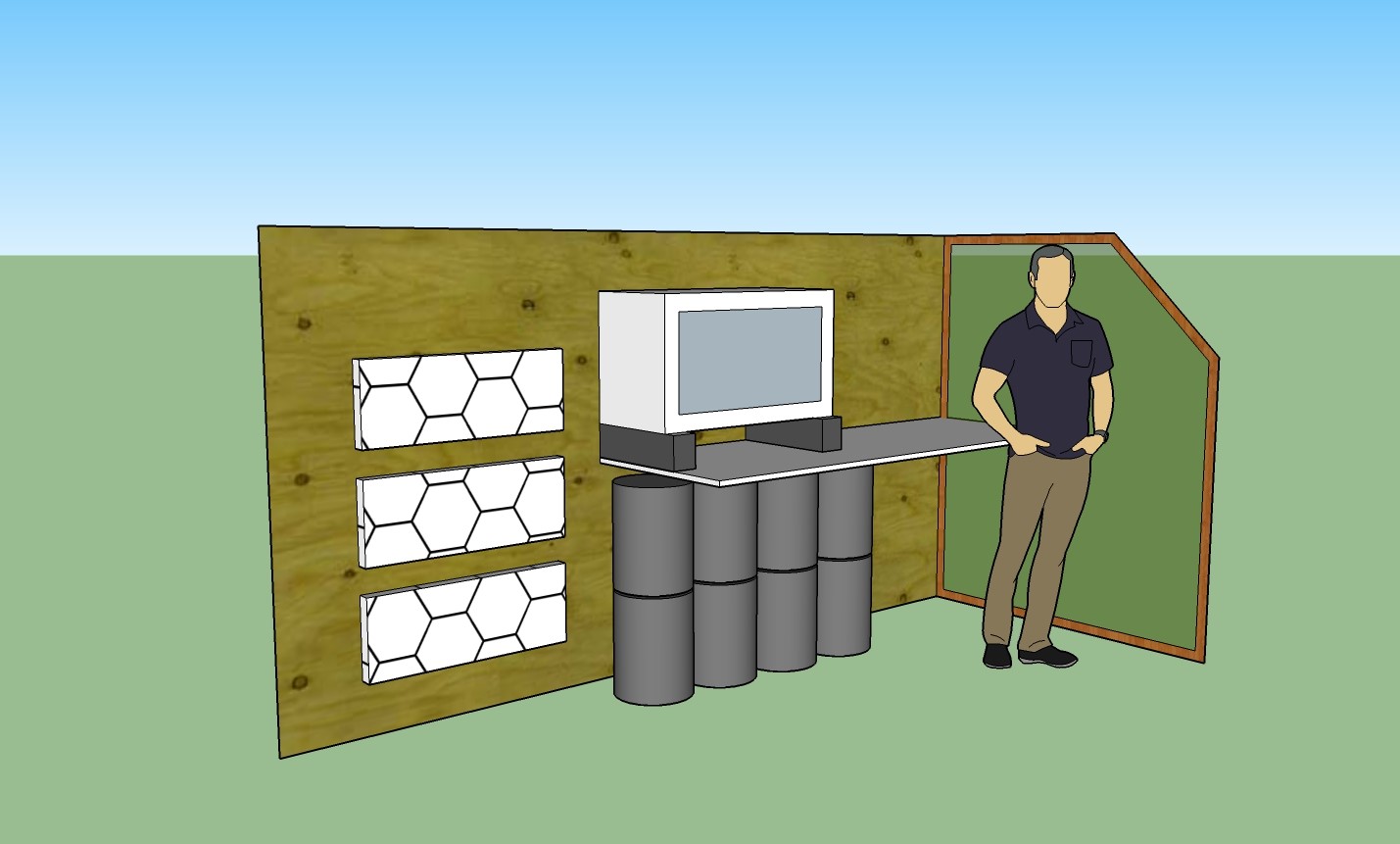

Above is the heat pump pipework. All the input to the tanks is via coils except the air side tank (on the left) which is direct. We’ll go through this, bit by bit, and you’ll see all the clever stuff emerge.

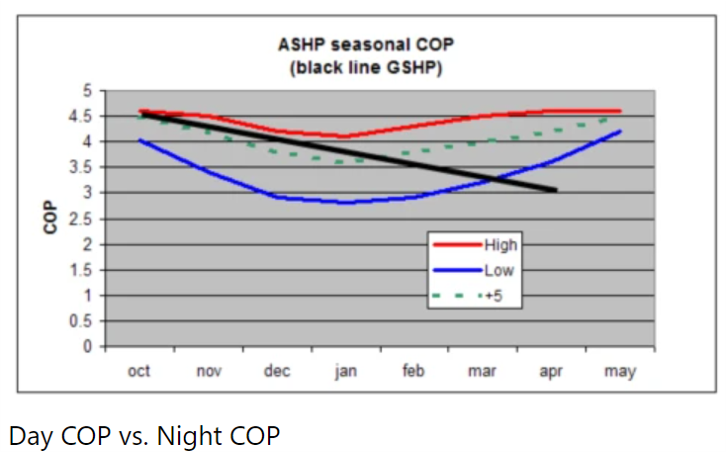

Running largely at night and avoiding all the cold air and defrosting malarky that would plague an ASHP a ground source pump is the starting point. GSHPs produce slightly better seasonal COPs than ASHPs but we can raise that even more by putting extra energy back into the ground.

Concept number one:

This chart compares the COP of a GSHP with the COP variation of an ASHP over the winter months. The daily swings in air temperature vary the COP of an ASHP hugely (the area between the red and blue lines) and show how day time running might be a lot better than night time. The black line for the GSHP is steady but declines as the ground is cooled by the season as well as the demand from the heat pump. Note the huge difference between the blue line and the black line which shows why ground source heat pumps are generally better.

Our system seeks to ignore that horrible blue line (i.e. don’t run the ASHP at night) and to operate around the red line and the black line. Those lines diverge after January where the ground gets colder and day time temperatures start to recover and it then makes sense to focus on daytime running of the ASHP. Here comes the big concept. We can also grab some of the day time warmth to benefit the GSHP and flatten and lift the black line to a COP of around 4. We do this with a tank and some air-to-water heat exchangers, shown on the left of the diagram above.

Here’s how it works. The outlet flow from the GSHP is typically around zero degrees, or colder, so the ambient air is nearly always warmer, especially during the daytime. The heat in the air is captured with three car type radiators and fans and circulated into the large buffer tank. This water goes to the ground loops whenever the heat pump and its circulation pump runs. There will be times when the tank is actually hot enough to feed energy back into the ground. Imagine a nice sunny day when the tank has been independently spooling up to 12c or so and the heat pump starts up and dumps 1,000 litres straight into the ground loops. This won’t happen often but the ground will rarely be fed temperatures below zero. Generally the ground loops will start off warmer and in warmer earth. The overall result is that we take a system that is intrinsically very good and make it much better. A higher COP gives much lower bills. A COP lift from 3 to 4 produces 33% more heat for your money; it’s that significant. That’s a good starting point but we can improve a lot more on that.

Concept number two:

Off-peak electricity can be had at night (for the car charging brigade) and when that is multiplied up by a heat pump the result is astonishingly cheap energy. A 10kW heat pump running 7 hours nightly for the whole 200 days of winter delivers 14,000kW.hrs for a mere £260. Crazy but true! The maths says it all; 7.5p for 1 kW.hr boosted by the COP makes 4kW.hr – divide 7.5 by 4 and you get 1.88p per kW.hr. How good is that? Well, gas is four times more expensive and direct electricity is twelve times more expensive, so yes, it’s good alright.

But it has to be stored ready for the next day, hence some tanks. Two 1,000 litre tanks for 2,000 litres of heating storage.

Although the ASHP is more suited for the day shift (nearer the red line on that COP chart) it makes sense to run it at night too when electricity is cheap. For example, near dawn while the GSHP tops up the domestic hot water cylinder the ASHP can be supplying much hotter water to the hot cylinder (red one on the right of the picture) for morning use on towel rails and fan-coils. The system can also be heating the concrete floor slabs at the same time so that’s more power used and stored.

Concept number three:

The stripper circuit

I developed this idea to preserve the precious heat in the hotter tank of a two tank system. It works a treat and will lift the performance of this system considerably. Here a three-port valve diverts water to the hot tank coil – if that incoming water is hotter – and the returning water then goes through the colder tank coil where the remaining heat is stripped out. If the incoming water is cooler than the hot tank then it is switched, by a simple Dt controller, directly to the cooler tank coil. So, if the supply from either heat pump was on a low set point, say to run the floors, then the hotter water tank, with its precious high grade heat, would be left undisturbed. That hotter tank could also be heated further by a wood burning stove or a gas boiler (directly, no coils) – and that’s where they go if needed. They say that you can’t combine low temperature heat pumps with additional high temperature sources but they are wrong – this does the job perfectly. A wood burner might be high on your wish list especially if you have access to cheap wood. A gas boiler is also a desirable addition to the stack of power sources, providing masses of high grade heat and adding to the overall system reliability.

Day time electricity is much more expensive but solar panels can help to run the ASHP fairly cheaply (or free) and that high, warm day, COP makes a big difference. Don’t forget, the stored energy might be enough to get through most days without any additional heat at all. That’s the benefit of having two lower powered heat pumps – you are more likely to be able to run one free on the solar panels. Of course, on really cold days both pumps can run together and along with any stored energy there will always be enough power.

Transmission

Lets now add a few more pipes to the two big tanks on the diagram. With masses of cheap heat parked in them, sending it to towel rails, fan coils in bedrooms, under-floor downstairs and in bathrooms is all easier than usual. All independent of the heat pumps and fully timed and zoned. If the diagram looks simplistic it’s because it really is that simple.

ESBE mixer unit

This blends down the big tanks to suit the under-floor pipes and it does weather compensation too. Normal UFH mixers are fixed at one temperature but ESBE mixers vary according to the outside temperature and adjust the power of the heating as necessary.

The towel rails and fan-coil units are separately fed by pump(s) and timers and there is no problem with zoning them as much as is required. If any radiators are used the hotter ASHP will cope with these too but they are best avoided.

Naysayers will now be saying that buffer tanks are inefficient or that heat pumps should run 24/7 or that zoning does not sit well with heat pumps. They are right on all counts but that misses the point; our system is so efficient and cheap to run it easily trumps any minor gains elsewhere.

The tanks – all from OSO

The tech room will look rather impressive with three 1,000 litre tanks. One will be for the air side of the hybrid heat pump and the other two for heat storage. A fourth tank is for domestic hot water. (300 litres with a 3msq coil for heat pump compatibility).

EDDI solar diverter

The GSHP can produce hot water cheaper than a direct immersion heater but the EDDI picks off solar excesses in short bursts during the day and runs the tank up to much higher temperatures. The heat pump will be all the better for not firing up all the time, the legionella will get regularly fried and a higher temperature effectively makes the tank size bigger; so wins all round.

Willis remote immersion heater

I like these because the circulation past the immersion element keeps the thermostat from shutting down under its own heat and also tank loading is straight into the top to maintain perfect stratification. Tank fitted immersion heaters can short cycle frequently and are harder to service too.

Air conditioning

Mmmm, how to mix heating the hot water cylinder with cooling the house? Easy actually; the GSHP and the Eddi do the hot water and the ASHP does the cooling of the floors etc. Both at once if you like. While this is technically possible I’d favour separate fan coil units which not only do cooling but add to the energy stack.

Solar panels + Enphase IQ8 micro-inverters

Each panel has its own micro-inverter for long term reliability, performance and also power if the grid fails – you know, in a Zombie Apocalypse scenario. At least 18 panels (about 7kWp) would often keep either heat pump running during the day. Each heat pump draws about 3kW so the panels should have that covered.

Electric car

It’s hard to get cheap off-peak electricity combined with a decent export rate so the car makes a good soak for any excess. You no longer buy petrol so that’s just as good as any export payments. N.B. There are no domestic batteries in our system – the money is better spent elsewhere. When the technology matures the car will be the battery anyway.

Solar tech room

This is just a fancy tweak – you don’t need this as part of the system; be cool if you did though.

All those car radiators and the ASHP would be neat and more efficient in a dedicated shed with glass sides for some solar heat. If possible, on a flat roof would be good. Apart from being neat and tidy the solar side helps to avoid the ASHP defrosting cycles with that bank of solar warmed water barrels. There is a COP lift too.

Summary

You’d need a huge house to justify all this but if you are in that fortunate position this maximises cheaper energy along with the versatility to cope with any demands. Some heat pump installations can be disappointing but this so simple and powerful there is no fear of that here, indeed you might have the best system ever devised.

Could this super cheap heating scale up for a really huge house? Absolutely, with reasonable capital costs and, with multiple power sources, better reliability too. Both heat pumps could go up to the next common size – 17kW each and then, if that’s still not enough, you could double up with two of each for a total of 68kW. More? Well, don’t forget that the hot tank is designed to receive direct heat from a gas boiler and/or a wood burning stove so if you need 100kW or more that’s no problem at all. E.G. Clearview 750 stove – 14kW plus Gas boiler – 30kW.

Compared with , say, a wood chip burning furnace this system is not only cheaper but easy to run reliably with lots of redundancy built in. Best of all though the extreme efficiency will get those bills down to levels you’d hardly believe.

There are a couple of significant heating ideas already featured on this site. One, the hybrid combined air/ground source heat pump, where a ground source pump has a connected tank warmed by the ambient air. And the other where big water tanks store cheap off-peak energy.

The first concept produces astonishing coefficients of performance and the second produces astonishingly low bills.

For the Grand Designs Heating System, we’ll combine these concepts and serve them up as a benchmark for what is possible. Here we go.

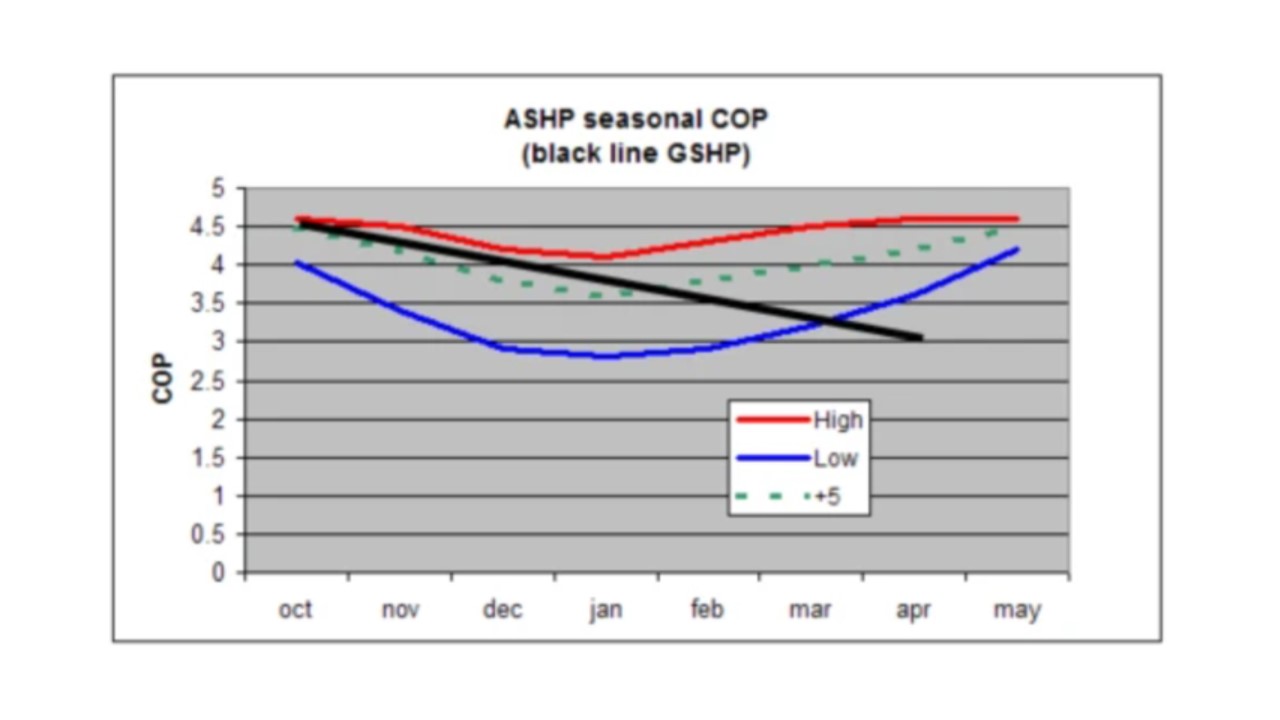

Running largely at night and avoiding all the cold air and defrosting malarky that would plague an ASHP. a ground source pump is the starting point. GSHPs produce slightly better seasonable COPs than ASHPs but we can raise the COP even more by putting extra energy back into the ground.

This chart compares the COP of a GSHP (black line) with the COP variation of an ASHP over the winter months. We can ignore that horrible blue line and focus on the divergence of the red line (warm air days) with the declining black line for the GSHP. Our mission is to grab some of the day time warmth and add it to the mix and thus flatten the black line to a COP of around 4. We do this with a tank and some air to water heat exchangers.

The outlet flow from the heat pump is typically around 0c or colder so the ambient air is nearly always warmer, especially during the daytime. The heat in the air is captured with three car type radiators and fans and stored in a large buffer tank. This water goes to the ground loops whenever the heat pump and its circulation pump runs. The design power of the radiator/fan combination is roughly equal to the heat pump to try to keep the ground temperature from depleting. There will be times when the tank is actually warm enough to feed energy back into the ground. Imagine a nice sunny day when the tank has been independently spooling up to 12c or so and the heat pump starts up and dumps 1,000 litres through the ground loops. This won’t happen often but the ground loops will rarely be fed temperatures below zero as is typical with most installations. The overall result is that we take a system that is intrinsically very good and make it much better. A higher COP gives much lower bills. That’s a good starting point but we can improve a lot more on that.

Concept number two:

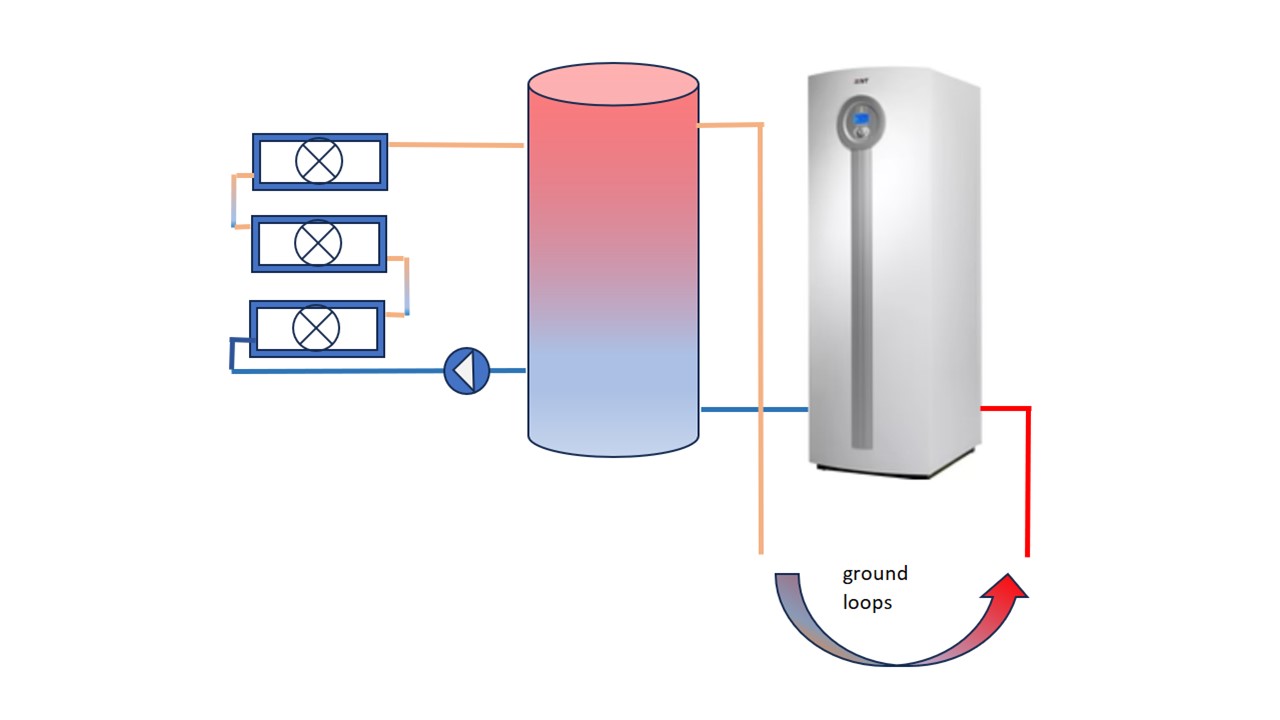

Off-peak electricity can be had at night, for the car charging brigade, and when that is multiplied up by a heat pump the result is astonishingly cheap energy. A 10kW heat pump running for 7 hours nightly over the whole 200 days of winter delivers 14,000kW.hrs for about £260. Crazy but true! The maths says it all; 7.5p for1 kW.hr on a COP of 4 makes 4kW.hrs – divide 7.5 by 4 and you get 1.88p per kW hour. Compare that with electricity which costs around 24p/kW.hr. The difference is astonishing but that cheap energy has to be stored ready for the next day, hence some tanks. Two 1,000 litre tanks combine to make 2,000 litres for the heating storage. N.B To remove that energy from the tanks we need to get the tank temperature back down to 30c or less and that will require, at least some, underfloor heating.

The stored energy might be enough to get through most days without any additional heat at all. If there is a shortfall any day time running will be much more expensive but the solar panels can help to run the GSHP fairly cheaply (or free) and that high COP makes a big difference.

Naysayers will now be saying that buffer tanks are inefficient or that heat pumps should run 24/7 or that zoning does not sit well with heat pumps. They are right on all counts but efficiency is not the point; we are using one third priced electricity which easily trumps any minor gains elsewhere.

The tanks – all from OSO

The tech room will look rather impressive with three 1,000 litre tanks and another smaller one. One will be for the air side of the hybrid heat pump and the other two for heat storage. The smaller tank is for domestic hot water. (300 litres with a 3msq coil for heat pump compatibility).

EDDI solar diverter

You could argue that the GSHP can produce hot water cheaper than a direct electric heater – the immersion – but the EDDI picks off solar excesses in short bursts during the day and runs the tank up to much higher temperatures. The heat pump will be all the better for not firing up all the time, the legionella will get regularly fried, and the tank size is effectively bigger; wins all round.

Willis remote immersion heater

I like these because the circulation past the immersion element keeps the thermostat from shutting down under its own heat. Tank fitted immersion heaters can short cycle frequently and are harder to service too.

Transmission

Towel rails, fan coils in bedrooms, under-floor downstairs and in bathrooms. All independent of the heat pump and fully timed and zoned. The big tanks make this possible and simple too.

ESBE blender unit

This blends down the big tanks to suit the under-floor pipes and it does weather compensation too. The towel rails and fan-coil units are directly fed by pump(s) and timers.

Mini-split

On warm days an air-to-air heat pump will be more efficient than the GSHP and it will be useful for topping up especially if it’s lower powered and often running free off solar. The blown warm air makes a useful laundry drier and the cooling feature sorts out the need for air conditioning. Cold air pours across the floors making a single source surprisingly effective.

Solar panels + Enphase IQ8 micro-inverters

Each panel will have its own micro inverter for long term reliability, performance and also power if the grid fails – you know, in a Zombie Apocalypse scenario. At least 18 panels (about 7kWp) would often keep either heat pump running during the day. The GSHP draws just over 2kW and the mini-split just under 2kW so the panels should have that covered.

Electric car

It’s hard to get cheap off-peak electricity combined with a decent export rate so the car makes a good soak for any excess. You no longer buy petrol so that’s just as good as any export payments. N.B. There are no domestic batteries in our system – the money is better spent elsewhere. When the technology matures the car will be the battery anyway.

Solar tech room

All those radiators and the mini split would be neat and more efficient in a dedicated solar shed. If possible, on the roof would be good. Apart from being neat and tidy the solar side helps the air powered mini-split to avoid defrosting cycles.

Conclusion

If you want your Grand Designs house to stand out and be the best of the best, this could be the way to go. What do you think Kevin?

BTW If you own a castle or something and this looks a bit light on, then check out the meaty version on

There is a hard push under way to make us abandon fossil fuel boilers and adopt heat pumps instead. The trouble is they don’t seem to work for everybody and they are expensive too. So, in many cases that’s a lot of money for something we don’t even want. Don’t despair though, there’s a way through this maze and the outcome could be cheaper heating for less initial outlay. The trick, in a nutshell, is to have more than one heat pump; the one they pay you £7,500 to install and then a smaller one to back it up.

Learn to love heat pumps

Typically consuming not much more power than an electric kettle the heat pump will deliver about 3 times as much energy to your heating, often more. The power is increasingly produced by renewables so the heat pump is an essential multiplier of green energy. That’s why we love them and that’s why we should have them.

Overcome the issues

Heat pumps work well at lower temperatures but that drastically reduces the effectiveness of your existing pipes and radiators. The pipes – usually 22mm copper – are the first bottleneck and probably only transmit around 12kW. So, without a total pipes overhaul the biggest heat pump you can have is 12kW (4kW drawn power). Half that, 6kW delivered is very common and suits well insulated modern houses and that might be the one for you too but only with extra back-up power.

Down the line the radiators will need an overhaul though; either some unsightly bigger ones or, preferably, fan-coil units with smart radiator valves on them to make heat distribution more selective and locally more effective. I prefer my own design for a DIY fan-coil unit (obvs).

With a smaller heat pump in the mix the chances are you can cover most of the cost with the £7,500 grant. A good start but now we need more power to back up a system living on the edge.

First things last

Before you start the big overhaul it’s best to install the back-up element, a mini-split heat pump – those aircon units often found in a hot foreign holiday rental. You probably only need one and they are so effective it should be a low power unit. The 1.71kW Mitsubishi SRK60ZSX-WF, for example, bangs out a healthy 6kW. Expect to spend under £2,000 for each one fully installed.

With the heat pump makeover done the running costs will still be the same as oil or gas but now the fun begins as we can move to the cost reduction phase.

First off, solar panels. Fitted with Enphase micro inverters you can fit odd numbers in odd places without any problems and they should give 20 years of trouble-free power. String inverters? Cheaper but when it fails in ten years everything fails at once; is the installer still around? Expect a long downtime, lots of grief and final expenditure higher than the Enphase route.

Because your heat pumps are low powered you will often find you can run one for free even when panel output is reduced. Include a solar diverter (like the Eddi) and the panels can send their surplus power to the immersion heater. This fixes the problem of poor hot water delivery associated with low temperature heat pumps and is the reason you might get away with not changing the tank in the first place. Keep your old tank, spend the money on panels. N.B the reason why your installer wants to change the tank is that the new one will have a much bigger coil to reduce recovery times – if you can afford it then go for it. Now the heating and electricity bills are usefully reduced and maybe servicing costs too. Do you service your fridge every year? No; same for heat pumps.

What about batteries? They used to be expensive and they wore out too quickly to justify the cost. But now they are cheaper (check out the Fogstar site) there is a better case for storing cheap off-peak electricity and running your (low powered) heat pump on it later. This can literally halve your energy bills – see graph below.

There’s a useful tactic to be considered when you are finally persuaded into owning an electric car.

Some EVs can offer 240v vehicle to load (V2L) with around 3kW available from a socket behind the back seat. They imagine you might plug in a toaster when you go camping. Never mind the toaster, you could plug in a mini-split and use cheap off-peak electricity to heat the house. If you are looking for a box of tricks to make this work check out the Victron Quattro-II which has an extra 240v input. The idea here is to go for a domestic battery first but be ready for the EV when it comes.

This all gets you connected to super cheap heating and air-conditioning too.

As you can see, cheap off-peak electricity, time shifted then multiplied with a heat pump gives astonishing results. Vehicle to Grid charging is another way although not yet mainstream but V2L gets us there now without installing the expensive V2G charger and you can choose from a bigger range of cars.So not a Nissan Leaf now, more likely a Kia or Hyundai.The result; half price for a lot of your heatingif not all of it.

The picture wouldn’t be complete without mentioning off-peak energy storage in water rather than batteries. Check out the idea in Grand Designs Heating System. Water lasts forever, batteries don’t.

Of course, all houses are different but hopefully there are some ideas here to help make a complex topic simpler. Small heat pump + mini-split + solar – the way to go – then batteries or tanks.